Maximusnd

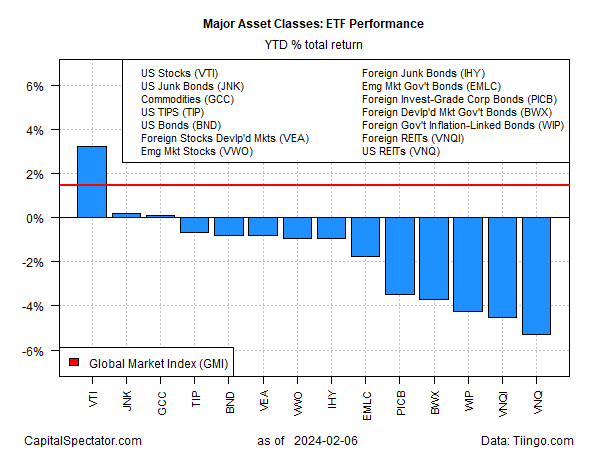

It’s lonely at the top. American shares are posting strong year-to-date results in 2024. Granted, it’s only early February. But the striking distance between the gain in US stocks vs. the rest of the major asset classes is still striking, based on ETF proxies through Tuesday’s close (Feb. 6).

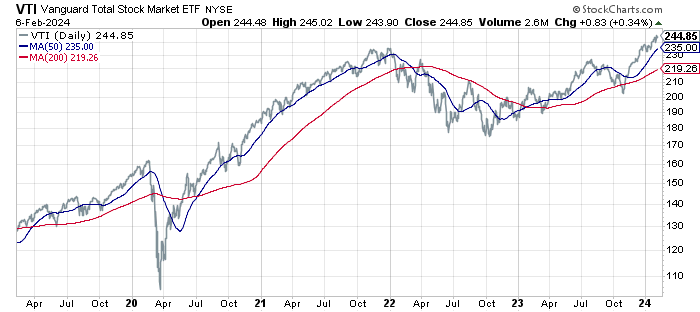

Vanguard Total US Stock Market Index Fund (VTI) is up 3.2% so far this year. That’s a stellar return, assuming it continued through the end of the year. That may be assuming too much, but for the moment the rise is all the more remarkable relative to the rest of the field, most of which are underwater.

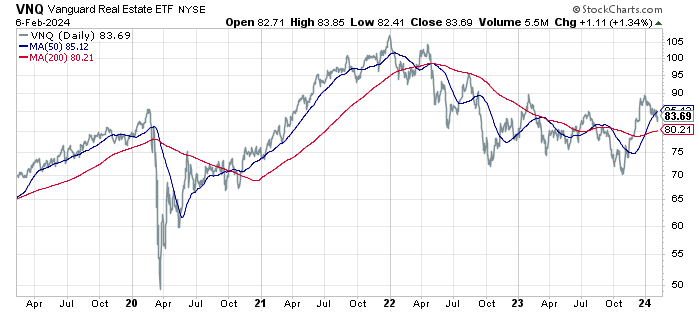

The biggest decline so far in 2024: US real estate investment trusts (REITs) via Vanguard Real Estate Index Fund (VNQ), which has shed 5.3% to date. Declining vacancies in office properties in the work-from-home era has become a weight on commercial real estate, which in turn is a headwind for VNQ.

Some analysts say the sector has become an intriguing value play after a rough ride over the past two years. VNQ’s trailing 12-month dividend yield is 4.16%, according to Morningstar, or slightly above the current 10-year Treasury yield. If VNQ can post even a modest gain over the next several years from current levels, the potential for solid performance is plausible.

The caveat is that it’s not yet obvious that VNQ’s negative momentum has run its course. The recent rally is reversing, and given the uncertainty about the office property outlook, there’s still a case for watching and waiting, at least for risk-averse investors.

The main question for asset allocation, of course, is how to deal with the hot run of US equities, which likely comprise above-average weights in many, perhaps most, portfolios. VTI is the upside opposite of VNQ as US shares continue to push into record-high terrain.

From a technical perspective, the strong bull run in American shares implies more of the same in the near term. Momentum tends to persist, until it doesn’t. Calling turning points in real time is tough, to say the least, and so the recent upside bias is arguably a positive forecast signal.

Yet, bulls need to keep in mind that the implied bet on letting the winners run is an assumption that big tech stocks can continue to drive the market higher. Note that while the SPDR S&P 500 ETF (SPY) is up nearly 4% so far this year, its equal-weighted counterpart (RSP) is flat. Removing the likes of Amazon (AMZN), Microsoft (MSFT) and other leading tech stocks paints a far less sizzling profile of recent market results.

“While elevated hedge fund positioning, numerous antitrust lawsuits from the DoJ and the FTC, and shifts in the macro regime will influence returns for the stocks, we believe that sales growth for the seven stocks will be the most important driver of the group,” writes David Kostin, chief US equity strategist at Goldman Sachs, regarding the influence of the so-called Magnificent 7 stocks.

The stakes are high for the market outlook, he advises. Indeed, rapid revenue growth will be crucial for ongoing leadership of so-called Magnificent 7 big-tech stocks that have been driving the US stock market’s rise.

Alas, the future’s still uncertain, leaving investors with the age-old question of how to position portfolios after such a lopsided run that’s favored one corner of the market?

Rather than trying to predict the future, perhaps it’s best to ask the baseline question: Why wouldn’t you rebalance now, if only on the margins, after such a lopsided run that overly favored one slice of the market over the rest?

As usual, your answer will depend on many factors, including risk tolerance, time horizon and various expectations, however flawed, for what’s likely to play out over the next year-plus. That’s a tough one, of course. What’s easy is recognizing you probably made a tidy profit due to a relatively narrow slice of global markets. The rest, as they say, is (probably) math if you look far enough into the future.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.